Getting accepted to university feels like a main character moment. You've picked your school, shared the screenshots, maybe started planning dorm décor or campus life, and then comes the less glamorous question: How is this all getting paid for?

If that question feels overwhelming, you're definitely not alone.

According to RBC research, more than half of students say they either use or plan to use financial aid to help pay for school. But while borrowing is incredibly common, understanding how it all works is another story.

Twenty-five percent of students using some sort of financial aid report having low confidence in understanding how student loans work, and only 28% feel very confident in estimating how long it could take to pay off their debt.

And honestly? That tracks.

The cost of university goes way beyond tuition. There are textbooks, rent or residence fees, meal plans, transportation, social plans and the random expenses nobody warns you about. Suddenly, the total price tag can feel a lot bigger — and a lot harder to predict — than it first seemed.

For many students, learning how to manage money and borrowing happens at the same time they're adjusting to an entirely new chapter of life. Which means figuring out finances isn't just part of the post-secondary experience; it is the post-secondary experience.

That's exactly why RBC created the Four Cs of Smart Student Borrowing — a simple way to help students feel more confident navigating how to pay for school and what borrowing really means.

Because figuring out finances shouldn't feel harder than midterm season.

Clarity: How much money do I actually need for university?

Studying adds up. Edwina Nava | Pexels

Studying adds up. Edwina Nava | Pexels

When students think about paying for school, tuition is usually the first number that comes to mind. But that's only part of the picture.

According to Statistics Canada, average undergraduate tuition for domestic students sits around $7,734 for the 2025/2026 academic year. But once you add housing, groceries, transportation, textbooks and everyday life into the mix, the total cost of a school year can climb past $30,000.

And those extra costs? They add up fast.

That's why getting clear on the full cost of school matters before borrowing decisions are made. Tools like RBC's Student Budget Calculator and Student Borrowing Guide can help students estimate what university life may actually cost.

Composition: What funding options are available to students?

Paying usually involves a combination of resources. Courtesy of RBC

Paying usually involves a combination of resources. Courtesy of RBC

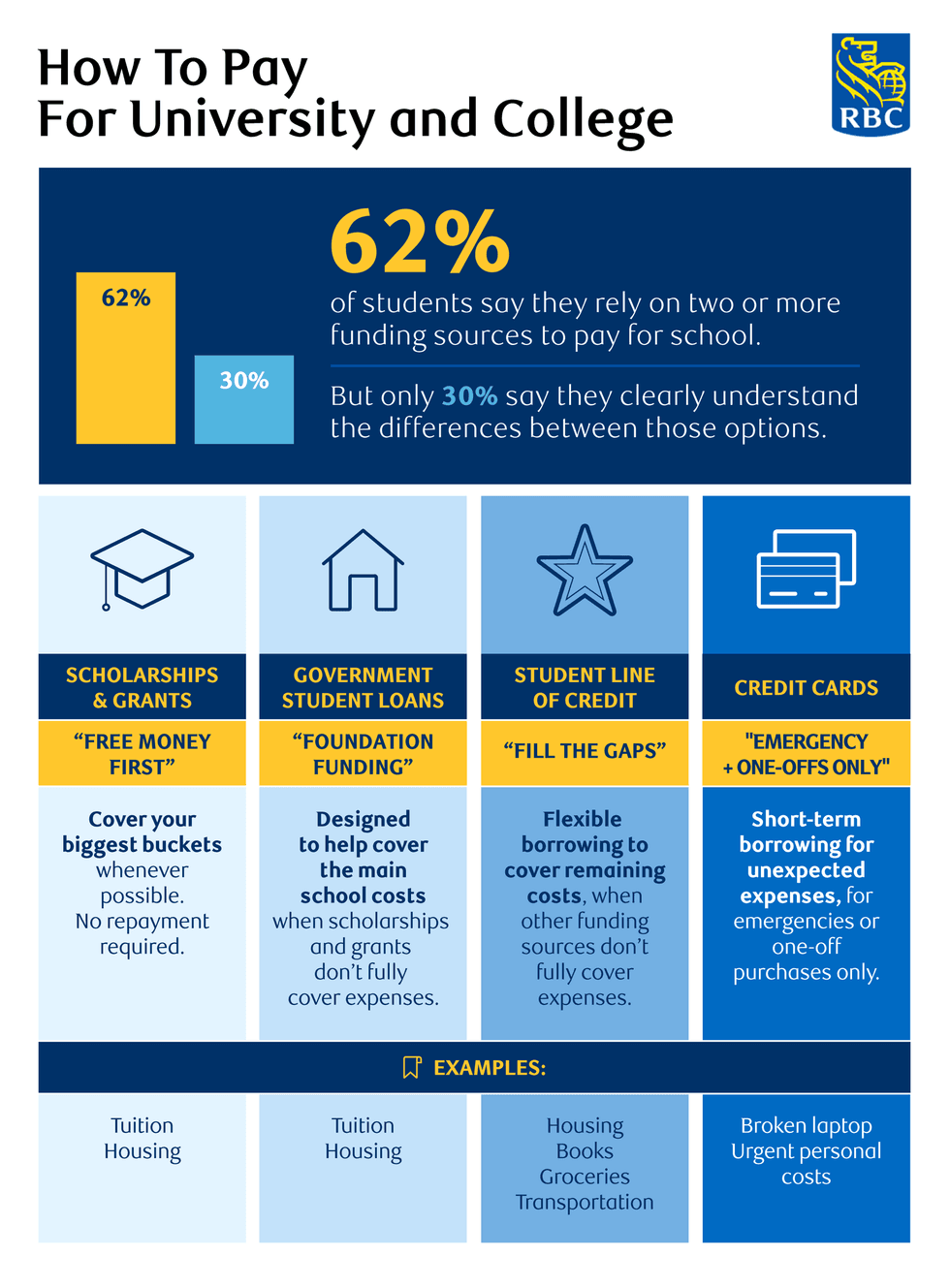

If paying for university feels like piecing together a financial puzzle, that's because for most students, it is. RBC found that 62% of students say they rely on two or more funding sources to help cover school costs.

Because every funding option works a little differently, understanding how they fit together can be just as important as understanding the costs themselves.

Cushion: Why some university costs are harder to plan for than others

You can still prepare for the unexpected. Fizkes | Dreamstime

You can still prepare for the unexpected. Fizkes | Dreamstime

There are some expenses students can usually predict. Tuition. Rent. Phone bills.

And then there are the ones that seem to show up out of nowhere. A laptop crashes during finals. A trip home becomes necessary. Suddenly, the budget you carefully planned in September looks very different by November.

That's part of why managing school costs can feel harder in real life than it does on paper. Building in some flexibility and expecting at least one surprise expense each semester can help create breathing room when things don't go according to plan.

Because sometimes financial progress looks less like having everything figured out and more like being prepared enough that one unexpected expense doesn't automatically land on a credit card.

Consequence: How do loans impact you after graduation?

Don't put off thinking about repayment. Kasto80 | Dreamstime

Don't put off thinking about repayment. Kasto80 | Dreamstime

Taking out a loan is one decision. Understanding what repayment looks like after graduation is another.

Many students say they aren't fully confident navigating things like interest rates, repayment timelines or how monthly payments work after school ends. That's why it can help to think about repayment while borrowing, not after.

Tools like RBC's What's Your Money Mindset quiz can help students better understand their spending habits, comfort with debt and financial decision-making style — all of which can make borrowing feel less intimidating and repayment planning more manageable.

Sometimes that means borrowing only what's needed for a semester instead of automatically taking the maximum available. Other times, it may mean paying a little extra when possible to help reduce interest over time.

The goal isn't perfection. It's making informed decisions with a clearer understanding of how today's choices can affect tomorrow.

The bottom line

Figuring out your unique situation is important. Armin Rimoldi | Pexels

Figuring out your unique situation is important. Armin Rimoldi | Pexels

There's no single "right" way to pay for university. But understanding how borrowing works can make those decisions feel a lot less overwhelming.

That's why RBC created the Four Cs of Smart Student Borrowing:

- Clarity: Understand the full cost of school beyond tuition alone.

- Composition: Learn how different funding sources can work together.

- Cushion: Build flexibility into your budget for unexpected costs.

- Consequence: Think about repayment at the same time as borrowing.

Because while paying for school can feel complicated, students shouldn't have to figure it all out alone.

To learn more about funding options for students, visit RBC's website.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. The information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.